Proven Risk Assessment Frameworks for Better Blackjack Betting Decisions

Human intuition is poorly calibrated for the kind of risk assessment that blackjack demands. We overweight recent outcomes, underestimate streak probabilities, and have no reliable internal mechanism for calculating expected value on the fly. The result is a pattern familiar to every experienced player: sound theoretical knowledge that dissolves under session pressure into gut-driven decisions that deviate from optimal strategy precisely when the stakes are highest. A structured risk framework is not a bureaucratic overlay on an otherwise intuitive game it is the replacement for intuition in the domain where intuition consistently fails. Professionals in finance, aviation, and medicine use explicit decision frameworks for the same reason: high-stakes environments require explicit protocols because cognitive shortcuts become expensive there.

Why Intuitive Risk Judgment Fails at the Table

Timeline

Step 1

Quantify Expected Value: Calculate EV per hand at current house edge and bet size before sitting down

Step 2

Set Variance Budget: Define maximum acceptable loss as a % of total bankroll for this session

Step 3

Identify Decision Rules: Pre-commit to strategy deviations (if any) based on count, not emotion

Step 4

Monitor in Real Time: Track units won/lost against your pre-set thresholds every 30 minutes

Step 5

Execute Exit Protocol: Walk when stop-loss or stop-win threshold is reached, regardless of momentum

How Does Expected Value Work as the Foundation of Every Decision?

Expected value is the weighted average of all possible outcomes of a decision. For a standard blackjack hand at 0.5% blackjack house edge with a $20 bet, the EV is -$0.10 per hand meaning that outcome is your expected loss per hand over a large sample. This number anchors every risk assessment. When you consider adding a side bet, the question becomes: what is the EV of that side bet compared to the main bet, and does the additional variance justify the additional expected loss? Most side bets carry 3–15% blackjack house edges, making them straightforward negative EV additions. The risk framework converts this from a vague sense that side bets are bad to a precise calculation that informs the decision with finality.

Risk-adjusted EV adds a variance penalty to raw expected value. Two bets with the same EV but different standard deviations are not equally attractive to a risk-constrained player. A $20 hand at 0.5% edge has expected loss of $0.10 with standard deviation around $20. A $200 parlay with the same mathematical EV has a standard deviation of $200. Both have the same EV, but the parlay carries ten times the variance which matters enormously when your session bankroll is finite and each outcome affects future decision-making capacity.

Risk assessment precedes every bet. The question is not whether you feel good about a wager it is whether the EV and variance are acceptable given your current bankroll and session objectives.

Framework Rule

How Do You Apply the Kelly Criterion to Bet Sizing?

The Kelly Criterion is the mathematically optimal bet-sizing formula for maximizing long-run bankroll growth given a known edge. Kelly bet = (edge × odds) / variance, simplified to edge / (odds against) for binary outcomes. For a card counter with a 1% edge at even money, the full Kelly bet is 1% of bankroll. This maximizes geometric growth rate while minimizing ruin probability in the long run. However, full Kelly generates high short-term variance, which is why fractional Kelly betting 25–50% of the Kelly-optimal amount is standard in practice. Half Kelly reduces expected growth rate slightly but cuts variance by 75%, dramatically reducing psychological pressure and the risk of a catastrophic downswing erasing the bankroll needed to continue playing.

Kelly Fraction

Relative Ruin Risk

- Very High

- Moderate

- Low

- Lowest

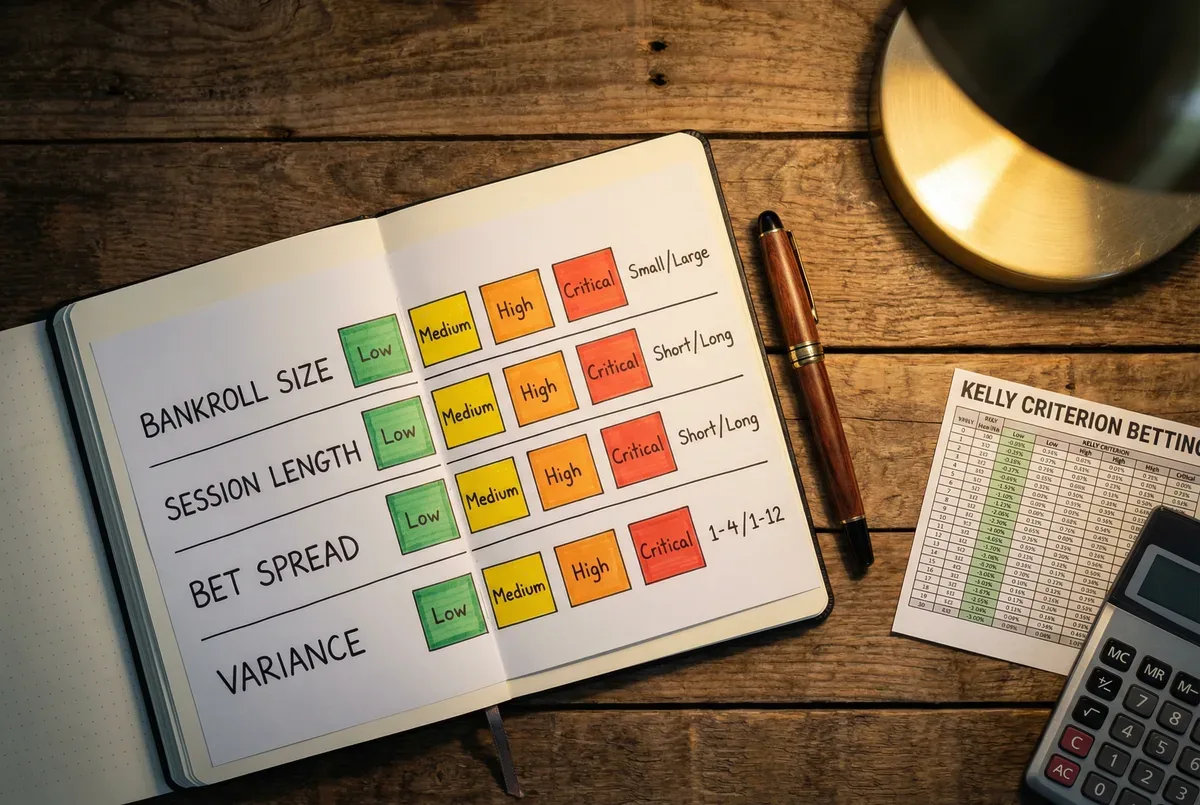

How Do Pre-Session Checklists Work as Risk Control Infrastructure?

Aviation uses pre-flight checklists because the cost of skipping a step is too high to rely on memory. The same logic applies to pre-session blackjack risk assessment. A five-minute checklist before sitting down covers: bankroll available for this session, unit size as percentage of bankroll, stop-loss threshold, stop-win threshold, target blackjack house edge of the game being played, and confirmation that blackjack basic strategy is fresh. This takes five minutes and prevents the single most expensive class of errors playing a suboptimal game because the conditions were never evaluated before buy-in.

Post-session review completes the framework loop. Recording actual outcomes against expected outcomes across multiple sessions reveals whether variance is behaving normally or whether strategy deviations are introducing systematic errors above the mathematical expectation. This is the only way to distinguish bad luck from bad play and the distinction determines whether corrective action is needed.

Pressure-Test Your Framework at Live Stakes

A framework that only works on paper is not a framework it is a theoretical exercise. The real test is whether you can execute your risk protocols when a losing streak triggers the urge to increase bets. Visit run this with real money at a live table under pressure and run three sessions with explicit pre-session checklists, mid-session monitoring checkpoints, and post-session logs. Real money stakes ensure the emotional pressure that makes frameworks necessary is present in full force. Review your logs after each session and note every point where the urge to deviate from protocol appeared and whether you held the discipline.

Frequently Asked Questions

Expected value per hand at your bet size and the prevailing house edge. Every other risk calculation variance, ruin probability, stop-loss sizing is built on this foundation. Without knowing EV, you cannot evaluate any risk parameter accurately.

Express your stop-loss as a percentage of your session bankroll. A 20-unit stop-loss on a 50-unit session bankroll means you are tolerating 40% drawdown before stopping. Compare this to the theoretical standard deviation of your expected loss over the session to verify it is appropriate for your risk tolerance.

It is relevant for any player sizing bets relative to a defined bankroll. Even recreational players benefit from the core Kelly insight: bet size should be proportional to edge and inversely proportional to variance. Full Kelly math is secondary; the principle of proportional bet sizing applies universally.

Before you test these plays at a real table, run them through our free blackjack simulator practice unlimited hands at zero cost until every move becomes automatic.

Mathematical Risk Warning

Risk frameworks reduce strategic error but cannot eliminate variance or house edge. All sessions carry the possibility of loss regardless of preparation quality. Never commit funds you cannot afford to lose.

Blackjack Academy is an educational resource. All strategy is based on mathematical expectation. Always play within your means.

Learn More

Continue your education with these related lessons.

Is the Match the Dealer Side Bet Ever Worth the Financial Risk

Match the Dealer pays when your initial cards match the dealer's upcard by rank or suit. The payout table looks…

Why You Should Always Start at the Table Minimum Bet

Starting at the table minimum is not a beginner's habit it is a professional protocol. Learn why experienced players invariably…

The Real Difference Between Replenishable and Static Gambling Funds

Not all gambling money is the same. Replenishable funds sourced from ongoing income behave differently from static capital in both…