Proven Methods for Managing Professional Blackjack Earnings and Reinvesting

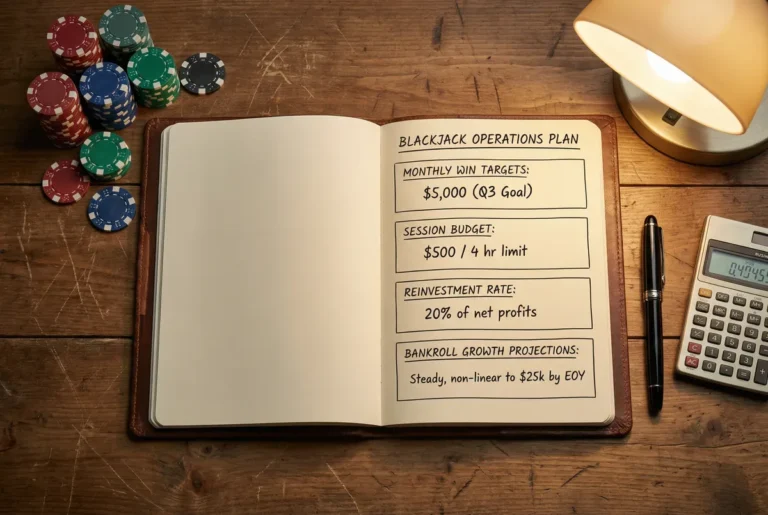

The most common financial mistake made by newly profitable advantage players is treating every dollar of winnings as available income. Winnings from blackjack serve three simultaneous purposes: personal income (which may be subject to tax obligations), bankroll replenishment after variance drawdowns, and strategic capital for bankroll growth that enables larger bet spreads over time. Treating all winnings as spendable income without allocating to bankroll reinvestment gradually erodes the capital base that makes professional play viable. A $5,000 winning month spent entirely on personal expenses leaves the bankroll exactly where it was before unable to support bet-size increases that would expand earning capacity in subsequent months. Professional income management requires a predefined allocation rule applied to every positive period, not just the months when discipline feels easy.

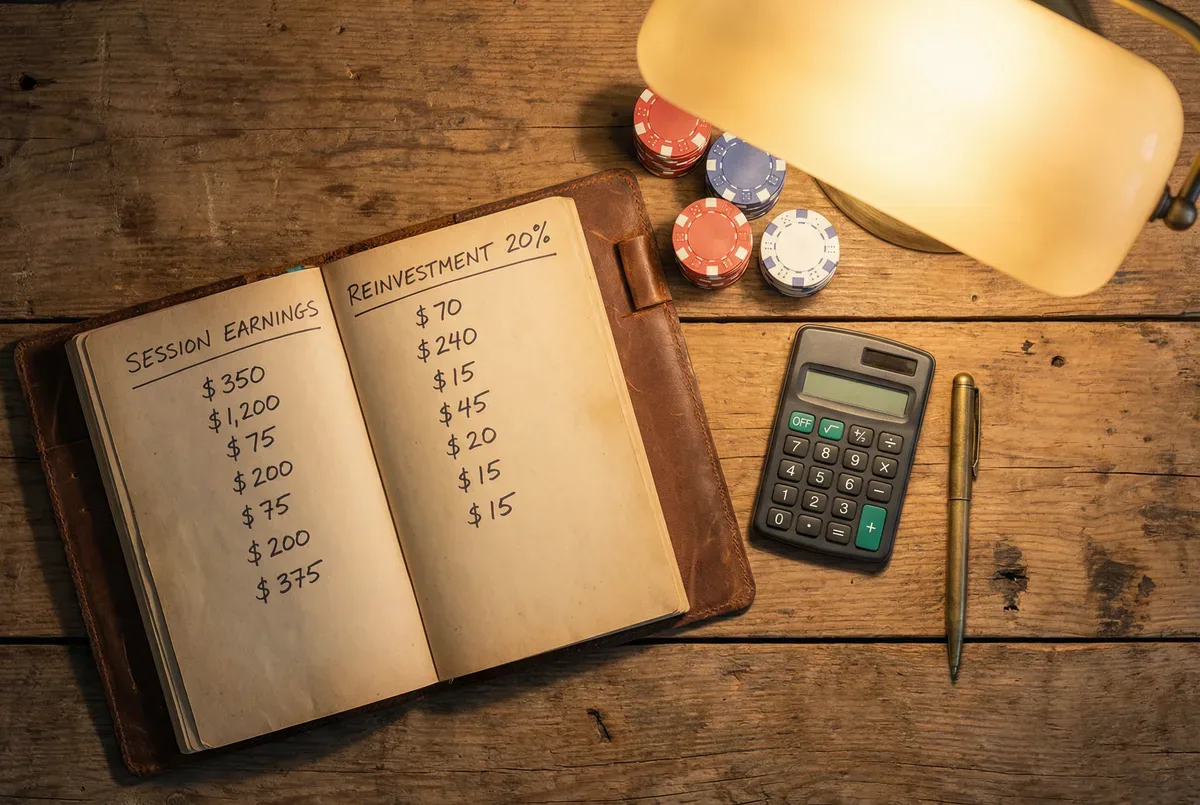

Winnings Are Not All Available for Withdrawal

- Tax reserveSet aside 25–30% of gross winnings before any other allocation

- Bankroll reinvestmentAllocate 40–50% of after-tax winnings to bankroll growth

- Operating costsBudget for travel, accommodation, tools, and training (10–15%)

- Personal incomeRemainder available for personal living expenses

What Is the Tax Obligations for Gambling Income?

In most jurisdictions, gambling winnings are taxable income. In the United States, gambling winnings must be reported as ordinary income regardless of whether a W-2G form is issued by the casino. Professional gamblers may file as self-employed, which allows deduction of gambling losses and operating expenses but requires quarterly estimated tax payments. The tax treatment differs materially between jurisdictions in the UK, gambling winnings are currently tax-free for recreational and professional players alike, while Canadian and Australian tax treatment is more nuanced and situation-dependent. The first professional session is the time to consult an accountant familiar with gambling income, not the end of the year when the tax liability has already been incurred without reserves.

Record-keeping for tax purposes requires the same session logs that bankroll management demands: date, casino or platform, session duration, starting and ending balance, and net result. These records support both self-reporting and, if audited, substantiation of reported figures. The IRS requires gamblers to maintain contemporaneous records retroactive reconstruction from memory is legally risky and practically unreliable.

Advantages

- Professional gambling status allows deduction of losses and operating expenses

- Detailed records provide legal protection in audit situations

- Quarterly tax payments prevent year-end cash crises

Disadvantages

- Self-employment tax adds 15.3% burden in the US on top of income tax

- Professional gambling status increases audit risk

- Consistent income documentation requirements add administrative overhead

What Is the Bankroll Reinvestment Strategy for Growth?

Bankroll reinvestment enables the bet-size increases that expand earning capacity over time. The Kelly-optimal growth strategy for a bankroll earning a 1% edge is to reinvest all profits and never withdraw until the bankroll reaches the next bet-size tier. In practice, most professional players adopt a modified approach: reinvest a defined percentage of after-tax winnings quarterly, withdraw the remainder for personal use. The reinvestment percentage should be calibrated so that the bankroll reaches each successive bet-size threshold within a defined timeframe typically two to three years between tier increases for semi-professional play.

The bankroll reinvestment discipline is hardest to maintain during strong winning periods precisely when it is most important. A three-month winning period that appears to have exceeded the bankroll growth requirement can evaporate in the subsequent three months of normal variance. Never withdraw from the bankroll in response to a winning period. Withdraw only according to your pre-set quarterly schedule.

How Do You Operat Costs of Professional Play?

Professional blackjack has operating costs that must be treated as business expenses before calculating personal income: travel to favorable game markets, accommodation, professional subscriptions (simulation software, counting training tools), books and educational materials, and potentially legal consultation. These costs reduce the net income available for personal distribution and bankroll reinvestment. Tracking them precisely allows accurate net-income calculation and, in jurisdictions where gambling operating expenses are deductible against gambling income, reduces taxable net profit.

Professional players who treat operating costs as personal expenses rather than business line items systematically underestimate their actual earnings and may under-invest in tools and training that have strong ROI in expected edge improvement. A $200 simulation software subscription that improves counting accuracy by 0.1% at a $5,000 monthly betting volume pays back in the first month of improved execution.

Build the Earnings Discipline From Your First Winning Session

Every discipline is easier to establish at the beginning of a practice than retroactively. After your first winning session at test this stake level at a live table immediately or any real-money venue, apply the allocation framework immediately even if the amounts are small. Set aside the tax reserve percentage, note the bankroll reinvestment allocation, and transfer only the personal income portion to your spending account. The habit of not treating winnings as purely personal income is the most important financial discipline a developing professional can establish, and it is dramatically easier to build from the first winning session than to introduce after months of full withdrawal.

Frequently Asked Questions

Yes. All gambling winnings are taxable as ordinary income in the US regardless of amount. Professional gamblers may qualify for self-employed status, allowing deduction of gambling losses and business expenses. Consult a tax professional familiar with gambling income before the end of your first winning year.

A target of 40–50% of after-tax winnings for bankroll reinvestment supports steady growth toward the next bet-size tier. The exact percentage depends on your current bankroll size, target bet-size tier, and personal income requirements.

In jurisdictions where gambling losses are deductible against winnings, legitimate operating expenses include travel to casinos, accommodation, professional software subscriptions, educational materials, and potentially professional consultation fees. Consult a tax professional for jurisdiction-specific guidance.

Before you test these plays at a real table, run them through our free blackjack simulator practice unlimited hands at zero cost until every move becomes automatic.

Mathematical Risk Warning

Professional gambling income is highly variable due to variance. Never rely solely on blackjack earnings for essential living expenses without maintaining adequate cash reserves from non-gambling income sources.

Blackjack Academy is an educational resource. All strategy is based on mathematical expectation. Always play within your means.

Learn More

Continue your education with these related lessons.

How to Handle a Large Blackjack Win at the Casino Cashier Safely

Winning big at blackjack is great until you handle it poorly. Learn when casinos report winnings, how to color up…

Why Treating Your Blackjack Bankroll Like a Business Beats Pure Gambling

Professional advantage players manage their bankroll with the same discipline as a small business separate accounts, profit-and-loss tracking, quarterly reviews,…

Why Past Hands Have No Effect on Your Future Results

Each blackjack hand is an independent statistical event. Past losses do not make future wins more likely, and winning streaks…